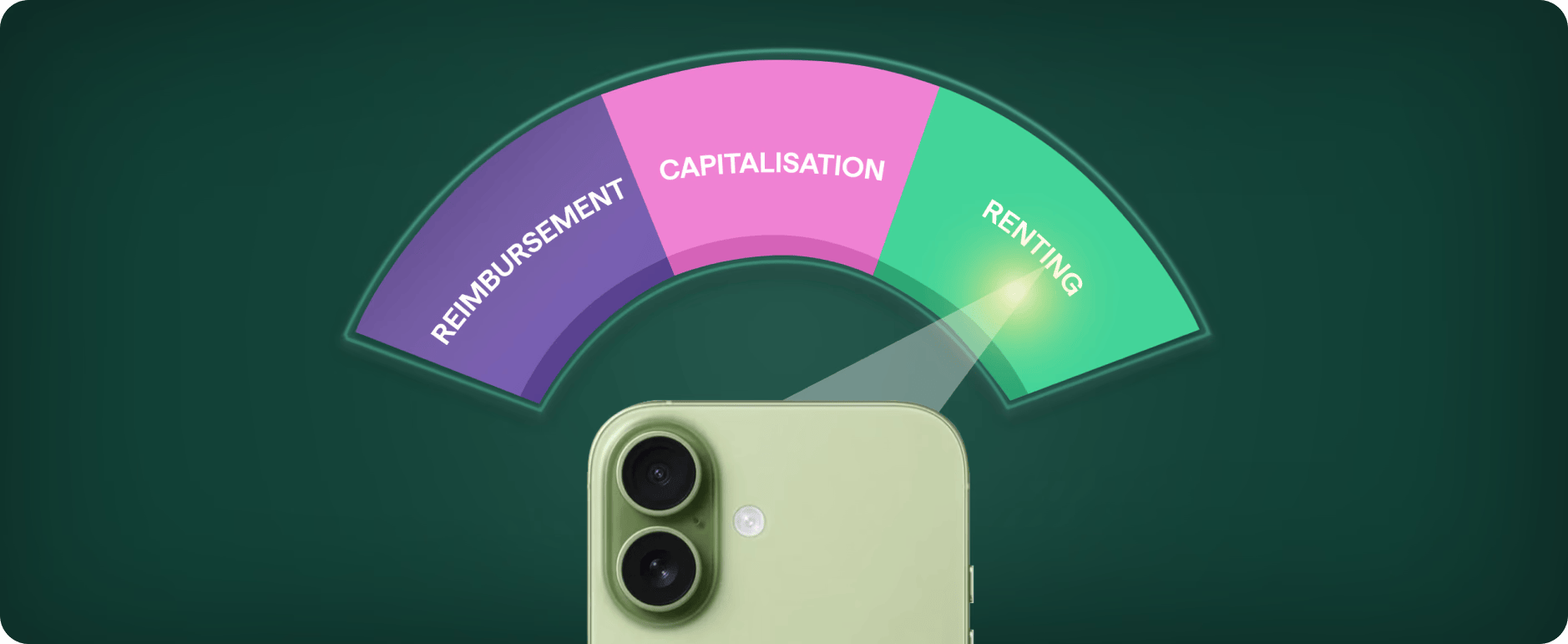

Reimbursement vs Capitalisation vs Renting: How Companies Should Really Think About Employee Devices

A Familiar Story: How it usually starts

Imagine a fast-growing company.

New hires are joining every month. Existing employees want better phones. Some need tablets. A few want accessories. HR wants to “do the right thing.” Finance wants compliance. Tax teams want zero surprises.

So the company asks a simple question:

“What’s the best way to give employees devices?”

Most organisations end up choosing one of three paths, often without realising the downstream consequences.

- Reimbursement

- Capitalisation

- Renting (Operating Lease)

They all sound similar. They are not.

This blog breaks down how each model actually works, where the tax and GST benefits really lie, and why renting has quietly become the most future-proof and compliant model for employee device benefits.

Let’s walk through each model, slowly, legally, and honestly.

The three models, at a glance

Before diving deep, here’s the conceptual difference:

| Model | Who buys the device | Who owns it initially | How cost is treated |

| Reimbursement | Employee (or company via employee) | Company | Capitalised asset |

| Capitalisation | Company | Company | Depreciated over years |

| Renting (Operating Lease) | Lessor | Lessor | Monthly operating expense |

The devil, however, lies in tax treatment, GST flow, and employee impact.

Model 1: Reimbursement: simple on paper, risky in reality

How reimbursement usually works

- Employee buys a device from the market

- Submits an invoice

- Company reimburses the amount

- Amount is adjusted against CTC or paid tax-free

Where problems begin

1. Capitalisation is mandatory

If the invoice is in the company’s name, the asset must be capitalised.

If it is not capitalised, the reimbursement becomes a taxable perquisite for the employee .

There is no middle ground.

2. Depreciation is painfully slow

- Phones, tablets, etc. depreciate at 15% WDV per year

- The company converts a 100% deductible salary expense into a long, thin depreciation trail

This increases corporate income tax liability in the first year.

3. Asset transfer creates perquisite tax

Under Section 17(2) of the Income-tax Act, any benefit provided by the employer that results in ownership or personal benefit to the employee is a perquisite, unless specifically exempt.

The problem:

- A reimbursed device becomes company-owned or employee-owned

- Either way, personal benefit exists

Under Rule 3 of the Income-tax Rules:

- Transfer of assets to employees attracts perquisite valuation

- Valuation depends on age of asset

| Asset Age | Perquisite Value |

| ≤ 12 months | 100% of cost |

| >12–24 months | 50% |

| >24–36 months | 25% |

| >36 months | 12.5% |

Employees end up paying TDS on something they thought was a “benefit”.

4. GST becomes a trap

- GST input on capitalised goods is spread over 5 years (20 quarters)

- On early transfer, GST must be reversed at 5% per remaining quarter

- A large portion of GST benefit is effectively lost

5. Fraud risk

Without a fixed B2B seller:

- Fake invoices

- Grey-market purchases

- Difficult audit verification

All become audit red flags.

Bottom line on reimbursement

What looks simple is:

- Tax-inefficient

- Audit-sensitive

- Employee-unfriendly

Model 2: Capitalisation: compliant, but economically inefficient

Some companies try to “fix” reimbursement by doing it properly.

How capitalisation works

- Company buys devices directly

- Assets are capitalised

- Depreciation claimed annually (usually 15% WDV for electronics)

- Devices are issued to employees for use

What still doesn’t work

- Cash flow heavy: upfront purchase

- Low expense recognition: only 15% depreciation allowed

- GST ITC lock-in for 60 months

- GST reversal risk on asset transfer

- Perquisite taxation still applies on transfer to employee

- Balance sheet bloat with fast-depreciating assets

Capitalisation is compliant, but financially inefficient for employee devices, which lose value rapidly and are hard to track as fixed assets.

Verdict on capitalisation

| Dimension | Outcome |

| Compliance | Yes |

| Tax efficiency | Poor |

| Balance sheet | Bloated |

| Employee experience | Rigid |

Model 3: Renting (Operating Lease): where structure meets efficiency

Now let’s look at renting the way it is actually designed to work.

How renting works

- Company leases devices from a leasing company

- Monthly lease rentals are paid by the Company

- Rentals are recovered from employees via salary sacrifice

- Ownership remains with the lessor during the lease

- Ownership never vests with employer

- Employee buys the device directly from the lessor at the end

Why this changes everything

1. Income-tax advantage (no perquisite)

Under Section 17(2):

- Perquisite arises only when employer provides ownership or benefit

In renting:

- Employer never owns the asset

- Employee buys directly from lessor at end

2. No capitalisation

- Devices never sit on the company’s balance sheet

- Entire lease rental is a valid business expense

3. Full GST benefit

- Lease rentals are services

- GST on lease invoices is fully available every month

- No 5-year lock-in

- No GST reversal on ownership transfer

This is one of the largest hidden advantages of renting.

4. Accounting advantage (Ind AS 116)

Under Ind AS 116:

- Leases ≤ 12 months qualify as short-term leases

- Allowed to be expensed straight-line

- No Right-of-Use asset

- No balance sheet impact

This is why 12 months is not arbitrary, it is intentional compliance design.

5. No perquisite tax

- Employer never owns the asset

- Employee purchases directly from the lessor

- No perquisite valuation arises at all

6. Real employee tax savings

- Lease rentals are deducted from pre-tax salary

- Income tax saved on the entire lease amount

7. Zero invoicing fraud

- Pure B2B invoicing

- Lease invoices come directly to the employer

- No employee-submitted bills

A side-by-side reality check

| Parameter | Reimbursement | Capitalisation | Renting |

| Balance sheet impact | Yes | Yes | No |

| GST efficiency | Poor | Poor | Excellent |

| Income-tax efficiency | Low | Low | High |

| Perquisite tax risk | High | High | Nil |

| Employee savings | Limited | Limited | Highest |

| Audit comfort | Low | Medium | High |

| Fraud risk | High | Low | Nil |

| Upfront cash | Yes | Yes | No |

| Balance sheet | Yes | Yes | No |

Why renting works better strategically, not just financially

Renting is not just a tax hack. It aligns with how modern organisations actually operate:

- Devices are tools, not assets

- Employees value flexibility over ownership

- Companies want clean books and predictable expenses

- HR wants choice, not one-size-fits-all provisioning

- Finance wants zero audit surprises

Renting aligns with:

- How tax law is written

- How GST credit is intended to flow

- How assets should be treated when value depreciates fast

- How employee benefits should work, flexible, optional, clean

It converts:

- Capital expense → Operating expense

- Asset risk → Service model

- Tax ambiguity → Tax certainty

The Tortoise perspective

At Tortoise, renting isn’t a workaround.

It is a deliberate design choice, because it:

- Maximises GST and income-tax efficiency

- Eliminates perquisite exposure

- Keeps employer balance sheets clean

- Gives employees real savings

- Scales without audit surprises

Final takeaway

If a company wants to:

- Zero perquisite tax

- Unlock real GST and income-tax savings

- Keep devices off the balance sheet

- Protect itself from audit and fraud risk

- Still give employees flexibility and ownership

Then renting (operating lease) is not just the better option.

It is the correct one.

Disclaimer

This article is for informational purposes only and does not constitute legal, tax, or accounting advice. Organisations should consult their professional advisors before implementation.

Founder & CEO

Vardhan Koshal is the Co Founder of Tortoise, India’s fastest growing employee device benefit platform. He has led India growth and product for companies like TripAdvisor and Udacity, and earlier founded Ridingo, a car pooling startup recognised by Forbes as one of the Hottest Global Startups and acquired by Carzonrent. At Tortoise he works with HR leaders, CFOs and tax experts to design compliant, high impact device benefit programs for Indian employers.